Why did Rio Tinto pay out $9 billion to shareholders in 2020?

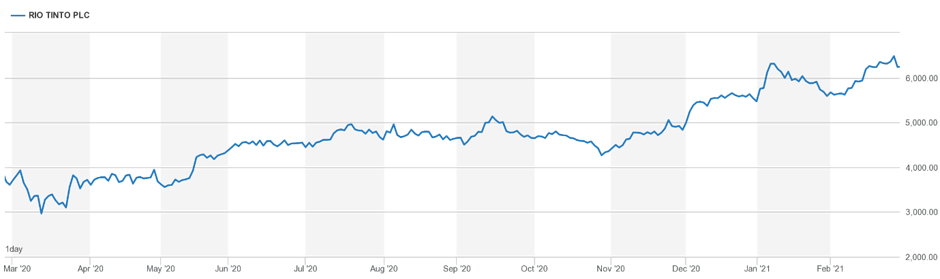

Mining giant Rio Tinto’s share price shot up last week, as they announced a record $9bn paid out in dividends to shareholders in 2020. This might seem counterintuitive in the context of a pandemic that has crippled the global economy.

Rio Tinto’s country busting dividend and related share price spike ban, however, be explained. It is due to the nature of the market the company operates in and a doctrine of shareholder primacy.

It is the later trend that we should see as a more fundamental threat to our way of life.

The stock market has done surprising well during what would appear to be a global economic collapse. Economics as taught at GCSE would suggest that the decline of real economy should hinder firms’ capacity to make profit, thus investors desire to invest with them. This has not happened.

This is partly as a result of individuals, funds and firms who have been lucky enough to retain their income during the pandemic accruing considerable savings over the course of Covid lockdowns. Some of this has since been invested in the stock market.

Alongside this, governments across the world – especially in the USA – have given their largest firms unprecedented public resources. In the USA and in the UK this has happened with little or no oversight. This has inflated a stock market that bares only a passing relationship to the real economy.

Additionally, certain large firms have done exceptionally well out of the pandemic. Think Amazon, Zoom, Astra Zeneca, Deloitte, and so on.

On the face of it, Rio Tinto would appear odd to be included as part of this group. It gains no direct benefit from contracts to deal with the pandemic response, nor does it exist in an industry that has ballooned by changes to life patterns triggered by Covid-19.

However, the price of iron ore, which makes up 90% of Rio Tinto’s earnings, is soaring – reaching levels not seen since the 2011 boom. This in part reflects speculation driven by the same savings glut and rampant inequality driving the stock market boom. However, there are also more fundamental reasons explaining the rising price of iron ore.

One of them is the lopsided nature of the recovery from Covid-19. While the West and South America is struggling, much of the Asia-Pacific has managed to reopen effectively. In China the economic recovery has been driven by a government stimulus that flowed heavily to the construction sector and delayed retirement of China’s excess steel melting capacity. This has boosted demand for steel and iron ore. Meanwhile supply is restricted by production delays in Brazil.

Moreover, the increased climate ambition around the world combined with the expansion of renewables necessitates considerable new infrastructure: expanded transmission, new wind turbines and so on. This will see increased steel demand and thus increased iron ore production: 64 million tons in the UK alone.

This explains the large profits Rio Tinto accrued in a year the global economy has been in chaos. But it does not explain the astonishing dividend payments.

The cult of the shareholder

Rio Tino’s dividend is remarkable not just for it’s size, but also for the proportion of earnings that it covers and that it comes after a major crisis at the firm. Rio Tinto’s last CEO resigned 6 months ago under a cloud after it’s mining operations destroyed an ancient sacred indigenous site. This is the latest in a list of practices campaigners have criticised regarding the company’s dealing with communities around it’s mining sites.

The dividend amounts to 72% of underlying earnings. A stakeholder view of the firm would suggest that various stakeholders have a claim on these earnings. These can range from workers, governments, and local communities whose lands they are using. These earnings can also be used to invest for future production and pay for innovation. The later seems particularly pertinent considering Rio Tinto’s own acknowledgement that it needs to decarbonise iron ore production.

Why with all these demands has such a large proportion of the firms profits being allowed to flow out the firm to shareholders?

Those of a more Marxist bent could suggest this is what corporations do. They extract value and resources from communities and workers at a profit and hand them over to those who own capital.

Others might point to management incentives. Modern management orthodoxy heavily ties management incentives not to long term profitability of the firm, or overall stakeholder satisfaction, but to shareholder interest and returns. Management who made the decision about where the surplus goes are heavily incentivised to reward shareholders. This is particularly the case for a new CEO.

Scholars like Lazonick have described how management theory has moved to reduce the corporation’s responsibility to it’s full range of stakeholders, to limit the fostering of innovation and instead pursue a laser like focus on delivering shareholder value. This encourages short term returns, share buy backs and a rising share price. It discourages sustainable community relations, long term investment, research and development into uncertain ends and building a skilled workforce.

What this means

This has consequences that go far beyond one firm and should worry us all. The justification for allowing the private sector to control much of our economy is that whatever the negative consequences regarding wealth and power distribution, it would allocate resources efficiently and the profit incentive would encourage new and innovative ways of doing things.

Facing the global biodiversity and climate crises with a need to adapt new ways of doing things and radically transform and decarbonise our infrastructure, we could certainly use some innovation and efficiency. Instead, firms are increasingly incentivised to focus on the short term, to take profits of extraction and return them to their owners rather than invest in the future. This means they perform their function of increasing inequality without performing their function of allocating capital productively. Instead more money goes to the global stock market casino.

This is not an insolvable problem, but it requires being willing to challenge the doctrine that firms are purely responsible to their shareholders. They should have a responsibility to wider society as well.

PS. We hope you enjoyed this article. Bright Green has got big plans for the future to publish many more articles like this. You can help make that happen. Please donate to Bright Green now.

PPS. Bright Green has an exciting series of events coming up. Join us for debates, interviews and much more.

Image credit: Ummatstef12 – Wikimedia Commons

“Those of a more Marxist bent could suggest this is what corporations do. They extract value and resources from communities and workers at a profit and hand them over to those who own capital.”

That isn’t Marxism, it’s National Socialism. You wrote that because you’re a NatSoc, whether you admit it to yourself or not.

Greens, why do you so consistently embrace tge far right?

Did you see the Great Reset writer’s latest opus (re)addresses benefits of stakeholder versus shareholder capitalism, almost as if it’s a new idea? Anything new will only be the genuine implementation of more economic equality. –

https://www.weforum.org/press/2021/01/klaus-schwab-releases-stakeholder-capitalism-making-the-case-for-a-global-economy-that-works-for-progress-people-and-planet/